Blog

Why Wall Street Dominates Placement-Agent Rankings — and Why Boutiques Still Matter

06/15/2026

Third-party marketers. Placement agents. Whatever term you use for them, 90% of firms don’t list a marketer on their EDGAR filings, clearly preferring to go it alone on the fundraising trail.

But for the 10% that do, plenty of marketing firms are doing something very right, because they help private fund investment managers raise billions of dollars of assets every year across the entire spectrum of asset classes and strategies.

As part of our process here at 9AT, our scouring of the Form ADV and Form D filings shows what would seem to be a huge 2,500 firms receiving a credential as a ‘marketer’ on regulatory filings, good for more than $21.68trn of gross asset value (GAV) in aggregate.

Leading the way are the investment banks. That should not be a surprise, as these firms are often helping to raise capital for the largest, most established alternative asset managers, and those mandates can be enormous. A single assignment for a multi-billion-dollar private equity, infrastructure or private credit fund can have a greater impact on rankings than numerous smaller mandates combined.

Add to that their longstanding relationships with their global network of investors, including pension funds, sovereign wealth funds and insurance companies, and the wider suite of advisory services they offer beyond capital raising, and it makes sense why these firms dominate the leaderboard, as can be seen from Table 1 below.

Table 1: Top 10 Third Party Marketers for Private Investment Funds, by Total Fund GAV*

Firm/Marketer | Total Gross Asset Value |

| MORGAN STANLEY | $ 942,011,984,267 |

| JPMORGAN CHASE | $ 933,620,411,662 |

| UBS GROUP | $ 915,207,040,644 |

| MIRAE ASSET | $ 824,372,342,544 |

| GOLDMAN SACHS | $ 582,078,583,510 |

| MITSUBISHI UFJ ALTERNATIVE INVESTMENT CO LTD. | $ 446,509,825,782 |

| BANK OF AMERICA | $ 444,116,913,829 |

| BARCLAYS | $ 396,654,165,981 |

| CITIGROUP | $ 359,064,457,932 |

| ICAPITAL | $ 259,192,007,320 |

Source: 9AT

*at June 24th, 2026

This dominance of large investment banks at the top of the rankings raises an obvious question, however: if global banks possess the scale, relationships and resources to lead the market, why do specialist third-party marketers continue to play such a prominent role in private markets fundraising?

The answer lies in a) the diverse needs of fund managers themselves and b) smaller and emerging managers being…too small and emerging for the bulge-bracket firms.

While the largest alternative asset managers may want and need global distribution capabilities, the long tail requires a more targeted, hands-on approach, which creates opportunities for boutique placement agents to carve out valuable niches.

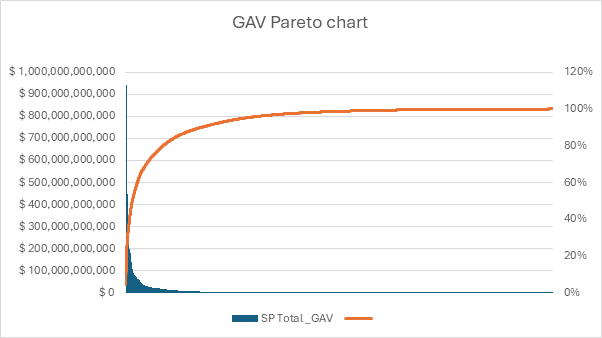

Indeed, the distribution of assets raised is quite skewed; as can be seen from the Pareto chart below (Figure 1), the aggregate GAV rises quickly before tailing off.

Figure 1: Cumulative Distribution of Aggregate Assets Raised by US Third-Party Marketers

Source: 9AT

While it’s true that this pattern is reflective of competition dynamics, it is also due to functional specialisation within the fundraising ecosystem. Boutique placement agents tend to operate where the large, global platforms are either structurally less efficient or economically less incentivised to focus their efforts.

For emerging and mid-market managers in particular, fundraising is often less about broad global distribution and more about precision: identifying the right subset of institutional investors, crafting a tightly aligned narrative, and maintaining close, consistent (but not overbearing!) engagement throughout the process. In this context, smaller third-party marketers can offer a level of focus and responsiveness that is difficult to replicate at scale.

Boutique firms are also often more deeply embedded in specific strategies, geographies, or investor networks particularly private investors such as family offices, multi-family offices, HNWIs, etc., enabling them to access capital that can meet quicker, respond quicker, and write a check quicker.

As a result, while the Pareto distribution highlights a highly concentrated top end of the market, it also obscures the more nuanced reality that the long tail of third-party marketing support is structurally important, sustained by specialist intermediaries that play a critical role in connecting capital with emerging and niche investment strategies.

Within the cohort of advisors that use marketers, private equity leads the way, and by quite a way – 43.3% of all funds using a marketer are private equity funds. That’s almost double the second-placed category – hedge funds – with 3,4560 funds, or 22.3%.

Table 2: Preponderance of Advisor Category Using a Marketer

| Category | Funds | Share |

| Private Equity | 6,696 | 43.3% |

| Hedge Fund | 3,450 | 22.3% |

| Venture Capital | 1,636 | 10.6% |

| Other | 1,599 | 10.3% |

| Real Estate | 1,081 | 7.0% |

| Securitized Asset | 984 | 6.4% |

| Liquidity | 35 | 0.2% |

Source: 9AT

Part of the reason would be that there are just more private equity funds that file to the EDGAR database. That in turn makes competition intense, and hiring dedicated expertise might be perceived as providing a capital raising edge. Plus, their larger size on average requires the target investor to be able to write a bigger check. That means less friends and family, more institutions, which is where placement agent relationships can shine.

Going back to the long tail shows us that for the 2,500 firms in our dataset, the 90th percentile is reached after only 423 firms, meaning that the remaining 2,077 support ‘just’ a couple of trillion dollars out of the $21.68trn total.

But those two trillion dollars are precisely where a) much of the innovation in private markets originates: first-time funds, specialist strategies, regional managers and emerging teams that collectively shape the next cycle of institutional allocation and b) niche capital raising relationships lie.

The majority of funds seem to be content with going down the DIY asset-raising route. But for those that aren’t – particularly new and emerging managers - there is clearly plenty of potential support out there.

Editor's Picks:

Here are a handful of articles that we’ve seen recently that we found interesting. Hopefully, you do, too!

- Hedge funds bet against European carmakers on Chinese competition fears

- Fewer LPs plan to increase allocations to private credit over next year

- Private equity bosses turn to carried interest loans as payouts stall

- Detroit Office CMBS: Limited Securitization, Divergent Credit Outcomes

- How to invest when everything is moving too fast